IMPACTfolio - 4th Quarter Newsletter

The 4th quarter of 2018 was bombarded with negative headlines that caused investor sentiment to swing to extreme fear. I started my financial services career in 1998 and I am still amazed how quickly the two emotions of “fear” or “greed” can quickly take over the market. No one really knows if this current sell-off will be short-term or long-term in nature. With experience, what I do know is that investors that stick with their well-crafted, long-term investment plans will be just fine. Investors that do not stick with their plan or allow emotions to start driving investment decisions will suffer and do more harm than good.

Negatives:

- Trade wars

- Brexit

- U.S. partial government shutdown

- Rising interest rates

- Quantitative tightening by the Fed reducing its balance sheet (similar to increasing rates)

- European Central Bank ending stimulus

- China slowdown (with or without trade wars)

- Earnings growth slowdown

Is the current sell-off the beginning of another “Great Recession” or worse the next “Great Depression”? We do not think so, we will share positive items in this newsletter to help provide perspective.

Positives:

- The price of oil has dropped over 40% since hitting a peak of about $76 a barrel in 2018. This generally means U.S. consumers are spending less money on gasoline and have more money to spend on other goods & services.

- The markets are hitting oversold levels that we have not seen since the end of the Great Recession in 2009. The NYSE Hi-Lo indicator is the ratio of stocks hitting new highs and lows (NYSE Hi-lo data provided by Dorsey Wright & Associates). The last time we saw it this low was an incredible buying opportunity. U.S. stocks hit a low in March 2009 and then rallied over 50% to end the year with a positive return of 26% in 2009 (S&P 500 index returns provided by Kwanti).

- We are not close to a recession in the U.S. when looking at Gross Domestic Product (GDP). GDP continues to be positive: 2nd quarter 2018 was 4.2% and 3rd quarter was 3.4%. A recession is defined as two negative GDP quarters in a row.

- The part of the yield curve that most economists follow has not inverted. An inverted yield curve simply means long-term rates on bonds are less than short-term rates. An inverted yield curve has preceded the past 7 recessions. When we compare the rates on short term treasury bonds (1yr and 2yr) with the rate on the 10yr, the slope is still upward. It has flattened over the past year, but it has not inverted.

- Investor sentiment is extremely bearish right now, which generally leads to good future returns. At the start of the year, investors were unequivocally greedy. And who could blame them? The S&P 500 had just completed its 9th straight up year and it did so without a pullback greater than 3%. In the AAII Sentiment Poll, Bulls outnumbered Bears by 44%. This was in the top 5% of all readings dating back to 1987. Fast forward to today and sentiment has shifted 180 degrees. Volatility has increased as the S&P 500 has experienced a pair of 10% corrections. In the same AAII Poll, Bears now outnumber Bulls by 22%, which is in the bottom 5% of all readings. Investors are now fearful.

What does this mean when it comes to markets? Extreme greed tends to be followed by below-average forward returns. Not in all cases, but more often than not.

But today, with extreme fear in place, the opposite tendency is observable. When investors are fearful, forward returns tend to improve, with above-average outcomes over the subsequent year.

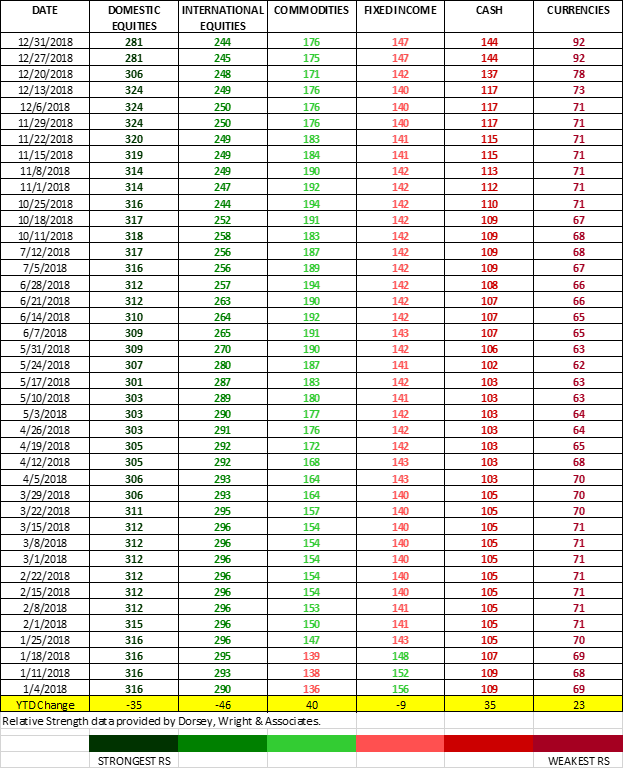

- The last item we will highlight is one of our favorite tools that allows us to see where the strength is in the markets, the Relative Strength Asset Class Comparison Chart. The current reading shows US Stocks in the #1 spot and defensive asset classes such as fixed income and cash in the #4 and #5 spots respectively.

The key takeaway with this quarter’s newsletter is that we will always see competing forces driving stock prices higher or lower. It is very easy to find data points for being bullish or bearish that may support your current feelings. The challenge during periods of losses is not letting your emotions sink your long-term plan.

Please contact us with any questions.

| Scott Arnold, CFP®, has been in the financial services industry since 1998. He is a co-founder of IMPACTfolio, a wealth management firm that specializes in IMPACT investing and holistic financial planning for one flat-fee. |

P.S. If you think this information would be of benefit to anyone you know, please share.